[RAM] RAM Ratings takes rating actions on Zamarad's Tranche 4, 6 and 7, and Al Dzahab's Tranche 6 sukuk

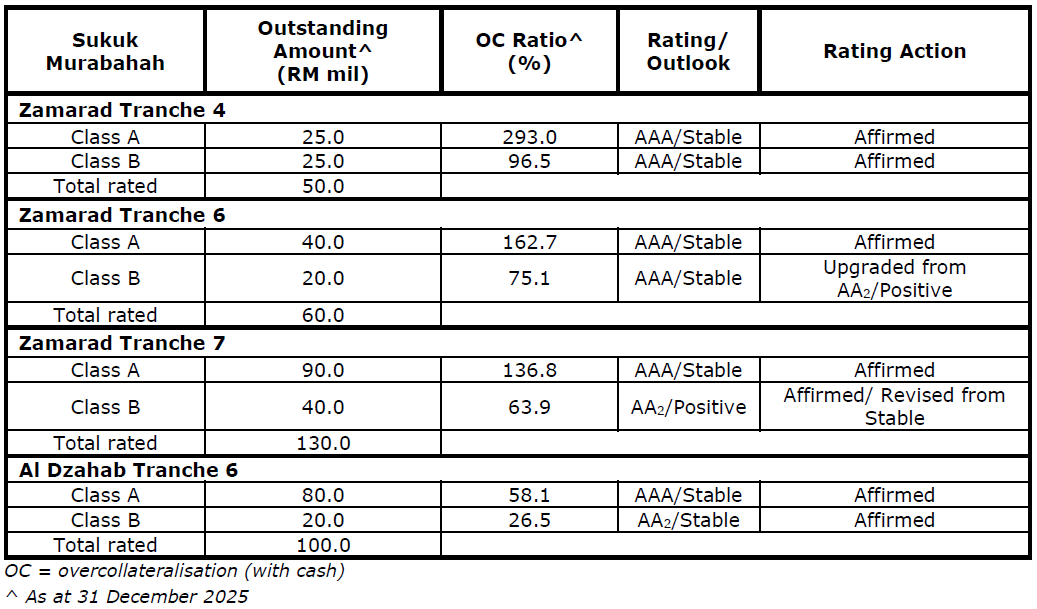

RAM Ratings has upgraded Zamarad Assets Berhad’s Tranche 6 Class B sukuk to AAA from AA2, and affirmed the ratings of all rated classes under Tranche 4 and 7 sukuk as well as Al Dzahab Assets Berhad’s Tranche 6 sukuk. Concurrently, the rating outlook on Zamarad’s Tranche 7 Class B sukuk has been revised to positive from stable (see table).

Al Dzahab and Zamarad are both special-purpose vehicles incorporated to undertake the securitisation of personal financing (PF) facilities extended to civil servants, originated through the business partners of RCE Marketing Sdn Bhd.

The rating upgrade of Zamarad’s Tranche 6 Class B sukuk is premised on credit support having strengthened to a level that commensurates with the AAA stress scenario. The rating affirmations reflect the underlying receivables’ satisfactory default and prepayment performances relative to our assumptions, providing credit support that commensurate with the respective issue ratings of all tranches under review. The positive outlook on Zamarad’s Tranche 7 Class B sukuk reflects our expectation that the available credit enhancement will support a higher rating over the next 12-15 months.

Zamarad’s Tranche 4 sukuk is fully cash-backed, the repayment of obligations under the sukuk are no longer dependent on future performance of the securitised receivables portfolio. For Zamarad’s Tranche 6 and Tranche 7 sukuk as well as Al Dzahab’s Tranche 6 sukuk, which feature a Revolving Option, any utilisation of excess cash reserves for the purchase of new receivables must at least preserve the required credit support for the respective ratings of the Class A and Class B sukuk, in line with the transaction terms.

During the review period, default performances across all portfolios were largely within expectations, despite some fluctuations attributable to collection timing and administrative delays during festive seasons. Considering the non-discretionary salary deductions through which the PF facilities are repaid and the low civil service attrition rate, default and delinquency levels are expected to remain stable. Average prepayment rates since issuance for the portfolios remained within our high and low scenarios. As prepayments are typically event-driven and tend to rise as the underlying PF receivables season, we anticipate a gradual increase in prepayment, driven by civil service salary adjustments and continued refinancing activity amid cost-of-living pressures, albeit within the range of our assumptions.

Analytical contacts

Tan Yan Choong

(603) 2708 8256

yanchoong@ram.com.my

Lim Chern Yit

(603) 2708 8302

chernyit@ram.com.my

Media contact

Sakinah Arifin

(603) 2708 8212

sakinah@ram.com.my